Real Estate

How to Get a Home Loan A Practical Guide to the Mortgage Process

April 21, 2026

Unlock the secrets to securing a home loan with our practical guide. Learn essential steps and tips to simplify your mortgage journey today!

Securing a mortgage involves numerous complexities ranging from various loan types to comprehending credit scores and interest rates. Each decision made can significantly impact your financial future. By taking the time to educate yourself about this intricate process, you empower yourself to make informed choices that align with your long-term financial objectives. This guide aims to clarify the steps involved in securing a home loan while providing valuable insights to simplify your journey into homeownership. Remember, understanding the mortgage landscape isn't just an advantage—it’s crucial for a successful investment.

What a Home Loan Really Means in Today’s Housing Market

A home loan, or mortgage, serves as a financial agreement enabling individuals to borrow money for purchasing a property. This process is fundamental as it empowers homeownership, which is a significant step toward building equity and enhancing one's financial future. In the current housing market, home loans are heavily influenced by fluctuating interest rates, which remain near historical lows, prompting many potential buyers to enter the market. However, in the face of rising inflation, lenders have tightened their approval criteria, resulting in varied approval rates and loan terms across different demographics.

Home loans come in diverse types tailored to meet various buyer needs. Conventional loans, known for competitive interest rates, typically require a higher credit score, making them ideal for those with strong credit histories. Conversely, FHA loans cater to first-time buyers with lower credit scores, offering them the chance to secure loans with minimal down payments. VA loans target veterans, providing favorable terms and often waiving the down payment requirement. Understanding these options is paramount for prospective buyers exploring today’s complex market.

Preparing Your Finances Before Applying for a Mortgage

Prior to embarking on the mortgage application journey, it's important to undertake specific financial preparations. Here’s a checklist designed for first-time homebuyers:

- Budgeting: Start by creating a comprehensive budget that outlines your monthly income and expenses. This will help you determine how much you can responsibly allocate to your mortgage payments. Factor in additional costs such as property taxes, homeowner’s insurance, and maintenance expenses to get a full financial picture.

- Saving for a Down Payment: If feasible, aim to save at least 20% of the home price as a down payment. This practice not only reduces your monthly payment burden but can often eliminate Private Mortgage Insurance (PMI). Consider establishing a dedicated savings account where you consistently deposit a portion of your income towards this goal.

- Review Your Credit Score: Your credit score is critical; obtaining a free credit report is wise. Check for any discrepancies and take steps to improve your score if necessary. Most conventional loans require a minimum score of 620, while some FHA options may be available to those with scores as low as 580.

- Clear Outstanding Debts: To improve your chances of securing a favorable mortgage, work on reducing your debt-to-income ratio. Prioritize paying down credit card balances and other loans.

- Document Financial Records: Collect essential documentation, including pay stubs, bank statements, and tax returns. Producing these records in advance can make the application process much more efficient and less overwhelming.

By diligently following these steps, you’ll place yourself in a better position to secure your mortgage and solidify the foundation for your future home purchase.

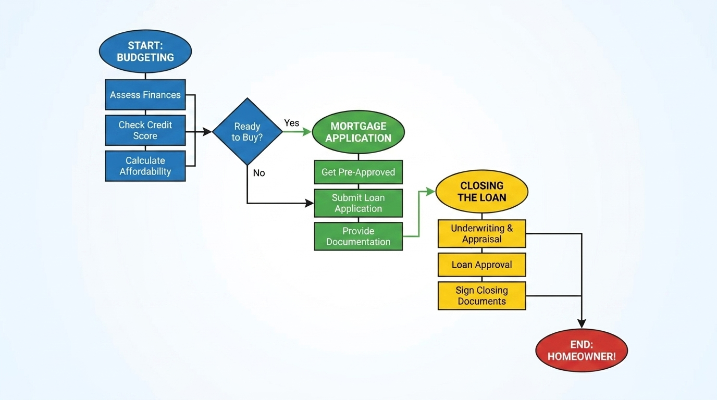

How to Get a Home Loan Step by Step

Obtaining a home loan may appear to be a challenging endeavor; however, breaking it down into manageable components can facilitate the process significantly. Here’s a thorough guide outlining each essential step in securing a mortgage from start to finish:

1. Select a Lender: Start your journey by researching various lenders, including banks, credit unions, and online mortgage providers. Compare interest rates, read customer service reviews, and examine the types of loans they offer. Pre-qualifying with multiple lenders allows for a clearer comparison of offers.

2. Prepare Your Finances: Prior to applying, assess your credit score as it has a significant impact on your proposed loan terms. Gather necessary documents such as income statements, tax returns, debts, and assets to streamline the application process.

3. Complete the Application: Once a lender is selected, you will need to fill out your mortgage application form. This document requires personal information, employment history, income, assets, and liabilities—provide thorough and accurate responses as any discrepancies may delay approval.

4. Provide Documentation: Expect to submit proof of income (including pay stubs and W-2 forms), details on your assets (like bank statements), and identification (such as your driver’s license and Social Security number). Each lender may have its own requirements, so clarify what each needs from you.

5. Loan Options: Familiarize yourself with different loan types available, such as fixed-rate mortgages, adjustable-rate mortgages (ARMs), and government-backed loans (FHA, VA). Assessing their advantages and disadvantages is essential to select the most suitable option based on your financial situation and desired longevity of occupancy.

6. Obtain Approval: After submission, be prepared for a waiting period as lenders may take several days to review your application. Upon approval, you should receive a Loan Estimate outlining the terms of your loan, including interest rates, associated fees, and estimated monthly payments.

7. Closing the Loan: Upon accepting the Loan Estimate, finalize arrangements with your lender to schedule a closing date. During this process, you will review and sign all necessary paperwork before receiving the keys to your new home. Don’t forget to conduct a final walkthrough of the property before making your commitment.

By thoroughly following these steps, you can approach the mortgage application process with newfound confidence. Seeking professional advice when necessary is essential, as it can save you both time and money in the long run.

Understanding Mortgage Approval Requirements

When seeking to secure a mortgage, grasping the common requirements can significantly bolster your chances of approval. To start, lenders often consider your credit score critically; a typical expectation is a score of at least 620 for conventional loans, while FHA loans might be obtainable with a score as low as 580. A higher credit score enhances both your approval likelihood and the prospect of favorable interest rates.

Equally important is your debt-to-income (DTI) ratio, which measures your monthly debt obligations against your gross monthly income. Generally, lenders prefer a DTI ratio below 43%. Maintain awareness that some lenders may approve higher DTI ratios if compensatory factors—like a robust credit score—are present.

Stability in employment history is another crucial expectation; lenders generally look for at least two years in the same position or industry, providing assurance of your ability to make consistent mortgage payments.

Importantly, lending requirements can vary significantly from one lender to another. Some may provide more flexible criteria, while others enforce stringent guidelines. It’s vital to compare options and understand these differences before settling on a lender.

Lastly, pursuing loan pre-approval can streamline your home-buying process. This action requires submitting relevant financial information so lenders can accurately evaluate your eligibility for a loan. Pre-approval signals to sellers that you are a serious buyer, further strengthening your position in the housing market. Gather necessary documents, such as pay stubs, tax returns, and bank statements, ahead of time and approach multiple lenders for comparative offers.

Common Mistakes That Can Delay Approval

Navigating the home loan approval process can be challenging, particularly for those buying a home for the first time. A common mistake is neglecting to provide required documentation; lenders require comprehensive financial details, and any missing or incomplete paperwork can significantly stall approval. Additionally, delaying the application—waiting until the last moment to start the process—can lead to rushed applications and potential errors.

Moreover, poor financial management—such as accruing new debt or failing to maintain steady income—can adversely affect your creditworthiness during the mortgage application journey. These pitfalls can delay your approval and diminish your chances of obtaining the loan altogether. By being proactive, organized, and financially astute, borrowers can sidestep these typical setbacks, allowing for a smoother and faster approval process.

Planning ahead and thoroughly understanding what lenders seek can ultimately save you considerable time and reduce stress, bringing you closer to achieving your dream of homeownership more quickly.

Your Path to Homeownership After Approval

Once your mortgage has received approval, the closing process represents the next pivotal step towards homeownership. This phase encompasses a series of actions culminating in the finalization of your property purchase. A closing date will be set, during which all involved parties—buyers, sellers, and lenders—will convene to conclude the transaction.

On closing day, be prepared for extensive paperwork. You’ll need to meticulously review and sign documents, including the mortgage agreement, title deed, and closing disclosure. Typically, a final inspection of your new home will occur to confirm it meets the agreed-upon conditions prior to transferring ownership. Finally, funds will be exchanged; your lender will dispatch the loan amount to the seller, marking the formal transfer of property ownership. While it’s common to feel a blend of excitement and anxiety, understanding this process can help demystify it and make the overall experience far more manageable for first-time buyers.

Empowering Yourself for Homeownership

Grasping the home loan process holds immense significance for first-time homebuyers navigating this often overwhelming journey. Equipping yourself with knowledge allows you to make informed decisions that align with your financial ambitions while alleviating anxiety and enhancing your confidence. Always remember that seeking professional advice—whether from mortgage advisors or financial consultants—can be invaluable in ensuring that every step you take remains strategically sound. Empower yourself to secure your desired home and establish financial stability for the years to come. With thorough preparation and the right guidance, your dream home is well within reach!

Just For You

Parenting

Baby Formula Feeding Chart An Essential Guide for New Parents

April 24, 2026

Pets

Potty Training a Puppy A Complete Guide for New Owners

May 29, 2026

Tourism

Best Hidden Gems in the United States 2026 Travel Guide

April 29, 2026

Shopping

Personalized Gifts for Grandma That Feel Thoughtful and Truly Meaningful

April 13, 2026

Recommended For You

Parenting

When Do Babies Sleep Through the Night A Comprehensive Guide for New Parents

May 7, 2026

Pets

The Importance of Cat Training

May 25, 2026

Tourism

Best Places to Travel Solo Safe and Inspiring Destinations

April 27, 2026

Shopping

Finding the Right Fit The Best Male Running Shoes That Balance Comfort, Support, and Performance

March 20, 2026